Translate this page into:

Exploring the Financial Toxicities of Patients with Locally Advanced Head and Neck Malignancies, Being Treated in a Private Sector Hospital in North India: A Thematic Analysis

Address for correspondence: Dr. Saurabh Joshi, KD 75, Pitampura, Delhi – 110 088, India. E-mail: soshijo@gmail.com

-

Received: ,

Accepted: ,

This is an open access journal, and articles are distributed under the terms of the Creative Commons Attribution-NonCommercial-ShareAlike 4.0 License, which allows others to remix, tweak, and build upon the work non-commercially, as long as appropriate credit is given and the new creations are licensed under the identical terms.

This article was originally published by Wolters Kluwer - Medknow and was migrated to Scientific Scholar after the change of Publisher.

Abstract

Background:

The high cost of cancer diagnosis and treatment is a global concern. Evidence derived, mostly from high-income countries, shows how it gradually impacts the personal and household financial condition causing the increased psychosocial burden of the patient and their families (termed “financial toxicity”).

Aim:

To qualitatively explore the financial toxicities in patients with advanced head and neck malignancies in India, and to consider how it impacts the patient and his family.

Methods:

Interviewing a purposive sample of 8 patients using semi-structured interviews face to face. Interviews were transcribed verbatim, and a thematic content analysis was carried out.

Results:

Four major themes were identified: burden and amplifying factors, impact, rescue and relieving factors, and learning and innovation. The burden of cost relates to diagnosis, treatment and non-medical costs which gets amplified while navigating the healthcare labyrinth. Emerging themes describe financial journey of cancer patients, the issues faced by them and the ways they tackle these issues during their treatment. Healthcare system factors like limited availability of adequate/comprehensive/meaningful insurance and reimbursements potentiate the toxicity. The financial toxicity leads to a significant adverse financial, psychological and social impact on the patient and the family. While moving through the process of care, there were a few learnings and innovations which patients proposed.

Conclusion:

This study provides qualitative evidence of the considerable and pervasive nature of financial toxicity in head and neck cancer patients in India. The findings have implications for all cancer patients and highlight the unmet need of psychosocial support for these patients.

Keywords

Financial planning

financial toxicity

goal based

health expenditure

insurance

palliative care

reimbursement

INTRODUCTION

Increasing incidence of cancer and the high cost of cancer diagnosis and treatment is a global concern. In India itself, the incidence of new cases is estimated to be 1.45 million each year, out of which approximately 30% of total cancer burden is constituted by Head and neck (H&N) cancers attributed to the widely prevalent tobacco consumption practices.[12345] Like all cancers, the diagnosis and treatment of H&N cancers place an economic burden on the family. 70%–90% of these are out of pocket expenses.[4] Of all H&N cancers in Delhi in the time period 2012–2014 (2552), 55% were in the economically productive age group of 25–60 years.[6] This cost burden gradually impacts the household financial condition and imposes psychosocial burden on the patients and their families. This economic change with its psychosocial consequences is termed as “financial toxicity.” The elements constituting this, may vary across different regions, cultures and family structures; and needs to be understood. Existing research, using various tools, has so far focused on high-income countries (HIC), with limited/no information from India. In India, where health insurance coverage is not a norm (unlike USA); and there are no social insurance frameworks set up like the NHS in the UK, the money-related toxicity may vary from those of the HICs.

A scoping review was done in March 2018 in PubMed for economic burden of cancer in India with no date or language restriction. Search strategy was ((“Cost of Illness”[Mesh] and “Neoplasms”[MeSH]) OR “Neoplasms/economics”[Mesh]) and India. Of the 110 studies identified, only six were relevant[789101112] and none of these had qualitative methodology. When we did a similar global scoping review to identify qualitative studies in this area as none were found in India, our search revealed 82 studies-(((“Cost of Illness”[MAJR]) and cancer) OR (“Neoplasms/economics”[MAJR])) and qualitative. 10 were relevant in cancer and qualitative context. All 10 were from HIC and focused on various cancers.[13141516171819202122] Out of this, we could get only one study from United Kingdom on H&N cancers, which mainly focused on caregiver perspectives.[14] We decided to explore this relatively under-researched area using a qualitative methodology. The aim of our study was to qualitatively explore the financial toxicities in patients with advanced H&N malignancies in India, and to consider how it impacts the patient and his family.

METHODOLOGY

Study design

The study was conducted in the oncology department of a tertiary care private sector cancer hospital in New Delhi, India, from August to December 2018; after taking ethical clearance from the institutional review board. Being a qualitative thematic analysis, purposive sampling was done. Indian, Hindi/English speaking patients between 25 and 60-years of age, diagnosed with H&N malignancy; who were also the main or the secondary earning members in the family, were planned to be chosen. They should have received at least 3 months of treatment, and were no >12 months-off treatment. Those who were unwilling or unable to provide consent, or had difficulty in speech and comprehension were excluded. After setting the criteria, the H&N Disease Management Group in the hospital was approached. They identified eligible patients by screening hospital case records. Eligible patients were then approached and explained about the study and given the information leaflet. They were given adequate time to go through the information, their queries were answered in subsequent outpatient visits and a written consent was obtained. The anticipated sample size was around 10–15. This was expected to increase or decrease based on saturation or emergence of themes after analysis of each interview.

Interview and data collection

The demographic details of patients were noted prior to interview, to get an idea of the socioeconomic status using Revised Kuppuswamy scale 2018.[2324] Researcher conducted an in-depth face-to-face interview using an interview guide, which were digitally recorded, anonymized and stored. Interview guide was formed basis the review of relevant literature and covered the financial experiences of cancer, descriptions of costs and reimbursements/insurances, the psychosocial, financial and spiritual impact of these costs. It also included, understanding the ways the obstacles were overcome, and whether the patients wished to make any relevant suggestions. Interviews lasted for around 30–45 min and were transcribed verbatim. The vernacular language interviews were translated and back translated to minimize any transcription/translation errors.

Data analysis

Patient recruitment stopped, once the new themes stopped emerging. The next step was familiarization with data, generating initial codes and identifying themes. Coding was manually executed on Microsoft word. Thereafter, the themes were reviewed, labeled to construct a meaningful data and final report was generated using this thematic analysis.[25] To minimize the bias which may arise from the researcher's background and life experiences, the researcher wrote down his prior experiences on the “cost of treatment in a private hospital” and reflexivity was used throughout.[252627] The analysis was done by first author and the transcripts were independently reviewed by two more authors. The coding was then done by consensus and important inputs from other researchers were utilized to ensure validity and reliability.

RESULTS

Eighteen patients were identified and out of them 15 could be contacted and 10 consented for the interview. Eight patients were interviewed as data saturation was achieved.Table 1 show the patient characteristics; majority of the patients were males (75%) and all except one patient belonged to upper or upper middle class.

| Participant | Age (year) | Gender | Cancer | Insurance/reimbursement | Kuppuswamy SES |

|---|---|---|---|---|---|

| P-1 | 60 | Male | Squamous cell carcinoma vocal cord | Private health insurance | Lower middle class (III) |

| P-2 | 52 | Male | Carcinoma right lateral border tongue | Government panel reimbursement | Upper middle class (II) |

| P-3 | 50 | Male | Carcinoma right buccal mucosa | Private health insurance | Upper class (I) |

| P-4 | 59 | Male | Gecurrent carcinoma right alveolus | Government panel reimbursement | Upper middle class (II) |

| P-5 | 56 | Male | Carcinoma right lateral border tongue | None | Upper middle class (II) |

| P-6 | 52 | Female | Carcinoma left lateral border tongue | None | Upper middle class (II) |

| P-7 | 50 | Female | Carcinoma supraglottic larynx | None | Upper middle class (II) |

| P-8 | 45 | Male | Carcinoma right lateral border tongue | Government panel reimbursement | Upper middle class (II) |

SES: Socioeconomic status

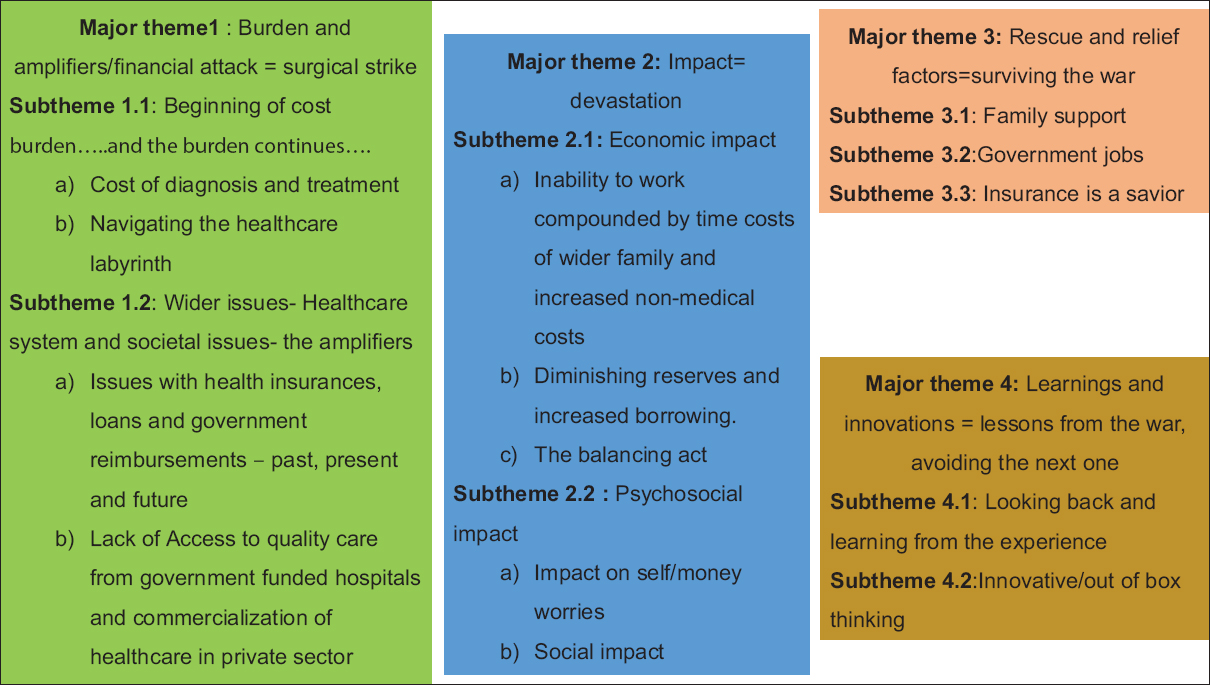

During the interviews, patients talked about their financial journey and its impact on them and their families, relationships within and outside the family, their positive and negative influencers, support systems, and also, the learnings and suggestions they gathered from this journey. First two themes [Figure 1] emerged around their negative experiences of battling with their finances. Next, two positive themes emerged around finding financial support, resilience and identifying new learnings from the skirmish. The experiences were more uniform in the negative themes; while the positive themes were reported by those who could preserve the positivity of their thoughts. For the sake of brevity and understanding; the results are discussed as major themes and sub themes.

- Themes and subthemes

Burden and amplifiers (financial attack/surgical strike)

Beginning of cost burden…and the burden continues…

The costs of initial diagnosis and treatment were reported as “exponentially high over a very short duration”, which plateaued afterwards, highlighting the initial lethal attack on financial capabilities, the massive efforts required to mobilize such finances and the intensity of suffering it generates [Figure 1-1.1.a].

…starting from the pre admission space.diagnosis, biopsy, the MRI, the PET scans.the tests.and the surgery and radiation together, I think I spend around 14 lacs…14 and half.maybe 15 lacs.you know.and the process…still on. 15000 rupees per month on my medications…tests.investigation which are going to happen in coming 6–8 months.minimum.so, the overall expense I think is somewhere between 15 and 18 lac…and I think spending 12 lakhs or 15 lacs in a duration of 3–4 months is very big.huge…10 times the average salary of middle-class person…(P-3)

…my cancer expenditure is too much and despite all the expenditures sufferings remain high (sad)…(P-1)

…just in case someone falls sick.he would lose/sell all fixed asset…(P-1)

…there is limited income in the family.there is no end to treatment expenses for cancer…household is affected a lot…(P-8)

Navigating the health-care labyrinth during multiple consultations at various places, in the initial and later periods; and the indecisiveness which persists during this time adds to the cost burden [Figure 1-1.1.b].

…I travelled from one doctor to another…went to so many doctors…and a lot of money have been spent on these…(P-7)

…facilities of cancer treatment are not available everywhere, so wherever they reach, they are already late for treatment…(P-5)

doctor says that you have to take 30 radiations.and then you study somewhere and somebody comes to you and says 30 is too much.it'll kill your body…and…drain your pocket…you need to have a second opinion or a third opinion…second and third opinions are always there…(P-3)

I was diagnosed with oral cancer at…Mumbai in 2016. Because of the delay in getting date of surgery.referred me to this hospital…(P-4)

Wider issues: Healthcare system and societal issues (the amplifiers)

Deficient societal inclination (for health finance) as well as the nonavailability in those earlier times, contributes to the inability to cover present day cancer care expenses for most people who are currently in their fourth decade of life or more. An average Indian family used to save for house, education and marriage; and life insurance and term insurance were more preferred than healthcare insurance. In addition, the uncertainty and lack of the timely and adequate availability of claims, lack of trust with insurance companies, tedious processes; and the need to bridge this “cost gap” with personal funds complicates the matter [Figure 1-1.2.a].

…and apart from a few insurance companies.which has just started 2–3 years back.there were not major players who gave you these kind of insurances.worth 40 or 50 lacs…where you could cover these kinds of.expenses. Generally, insurance companies…were offering you 3 or 5 lacs or maximum 7–8 lacs as a floater.you didn't have many avenues…(P-3)

…when I was 20–25 years old, I could not imagine myself to go for…10–15 lacs…for medical insurance. At that time there used to be term insurances…and the life insurance used to be more important than medical insurance.now when you ask.if I could do it.realizing that the cost of medicine or medical care has gone up…not available.because of the preexisting diseases.sugar, BP…so.at 40–45 years…getting your insurance which covers your existing or preexisting diseases.is difficult…India as a society.saves money for only two three purposes.one is the higher education.second is the marriage in the family.and third is to construct a house.nobody makes a saving for health…(P-3)

We would get insurance claims after the completion of treatment…it is difficult…So far, they have given only 1.5 lakh rupees…not received the complete payment…so we had to deposit…from our pocket…(P-1)

…insurance helps if you know someone in the company…(P-6)

Lack of access to quality care from government funded hospitals (lot of paperwork, casual attitude, and long waiting times) and commercialization of healthcare in private sector (lack of compassion and appropriate guidance, unmet expectations of relief despite huge spending reportedly increased the-life versus money struggle [Figure 1-1.2.b].

…I would have been lying in a poor government run facility…would have accepted whatever kind of treatment I have received could not have lived for 2 years, would have lived for 5–6 months.(P-4)

government hospitals.long queues.long waiting times. 5–6 months for starting the treatment after you get enrolled.(P-8)

… we have converted this into an industry.we see people doing medical tourism here, we think that we are going through a hotel and not to a hospital (eyes wet). I can understand that hospitality and Hospital business, both are businesses, but there has to be a difference…(P-3)

Impact (the devastation)

Economic impact

Inability to work was compounded by time costs of wider family and increased nonmedical costs, for example, travel, food, and stay; and visitor subsistence [Figure 1-2.1.a].

expenses of treatment…room rent, medicinal costs, the expenses for travelling and living of the attendant who stays with me, whoever comes from Varanasi and travel to see me would also be spending a lot…(P-5)

but someone who is not able to work…is not paid for the days he takes off work…(P-2)

…it is very troublesome…not only physical problems…also, the time, traveling, lodging, food…(P-1)

Financial reserves diminish and borrowing increases, as the financial burden coerces the patients to procure informal/formal loans and exhaust savings, causing medical bankruptcy. Patients from outside the town need to maintain multiple accommodations [Figure 1-2.1.b].

…I need to deposit it for my treatment…so I have taken loans from my relatives and friends…(P-1)

I used my savings from mutual funds and other instruments for child's education…for paying their education and hostel fee…(P-2)

I had my provident fund.and I used it since I had to pay college fee for my daughter.that was my 25–30 year savings…(P-8)

…rentals incurred from two accommodations needed at two places.there (Allahabad) and here (Delhi)…(P-4)

Burdened with expenses, the balancing act starts, for example, reduction in leisure/recreation/outings, using cheaper but inconvenient and crowded modes of transport (exposes to infection), reducing the sharing of joy with family; and all this leaves a sense of guilt [Figure 1-2.1.c].

…for getting through the treatment…we have reduced some family expenses…manage family budget…use cheaper transport modes…(P-1)

…use to go for a family dinner every 10–15 days which we have now reduced to once a month…we have also reduced children's outings and holidays…(low mood)…(P-2)

Psychosocial impact

A complex interplay of symptoms and financial challenges e.g., child's marriage expense, wider family's spending, mortgage, people taking undue advantage, loss of job and employability adds to the worries. Financial dependence is perceived as a threat to moral identity, for example, when enquired whether government panel reimbursements are benefits provided by the employers; it is quickly denied, rather the interviewer is made to understand by specifically pointing out, that, these were entitlements, not hand-outs/benefits [Figure 1-2.2.a].

I am unable to eat…very painful…I vomit at times…lot of secretions in the throat…leave my food as it is…I am fine for 2–3 days after the chemotherapy…and thereafter a lot of things happen…I become weak and fatigued…and then the cost (eyes wet)…(P-1)

I wish to get my younger son married…need money for that also…(P-1)

one (son) is doing hotel management from the university and other is studying…he has his exams this year (looks anxious)…(P-5)

he (son) has just finished studying…was supposed to appear for job interviews…but he is looking after me…he is the only child…(P-7)

No (very strongly)…not at all.it's not a facility it is a rule…it is an entitlement we are eligible for.as Government employees.(P-8)

certainly.a lot.you don't have to beg…withdraw your money and spend on your treatment…(P-8)

An intentional/unintentional lack of support and abandonment creeps in, and parents felt hesitant to ask their children for financial needs, unless offered by children themselves especially if children were staying away with their families and were not in a joint family system. Some people took undue advantage, friends turned foe and tried to reap benefits [Figure 1-2.2.b].

…not easy to ask for help; the person whom you ask for help “pity you”…(P-2)

I don't have an accommodation of mine. I have lost all my property and money to cheats (mentioned some relatives)…(P-4)

…they (daughters) have their own expenses.their own family.their kids…I am unable to ask them…(P-4)

no one helps you in the bad times…even your children prefer to stay away…if you have the money.people would definitely come and see you intermittently…(P-4)

If we ask for help and people see we are in need…they might lend us loan on higher interest rates…people try to reap benefits from you when you are in difficulty…am worried…lot of difficulties…(P-2)

Participants reported a broad range of complexities of financial distress and the knock-on effects to the individual psyche, intimate familial relations and money worries [continued on Table 2].

| Psychosocial impact (contd.) Psychosocial impact |

|

|---|---|

| The realisation that finances guide treatment (allopathy vs alternative medicine), loss of control over expenses, existential distress and, financial misery of fellow families, creates a negative impact. Survivors are busy managing the financial aftermath of cancer till they are alive [Figure 1-2.2.a]. |

the differential between the price of an allopathic…compared to.naturopathy…so huge that people are bound to go that (naturopathy) way…which I think.may not be.that good…that favourable (sad)…(P-3) a relative of mine going to the same trauma…waiting for another surgery…nobody in the family…help them…lastly what they did was…opted for some naturopathy…whatever they have saved for their last days is no more available…(P-3). everything is mismanaged. and out of control…(P-4) I don’t have anything to think about.what should I think.(crying)…whatever time I spend with my wife is my life. I never earned black money…why me…I have worked with honesty…(P-4) And probably I would be paying that Insurance…for…till I live, to pay the cost of what they have incurred on me (Disappointed)…(P-3) |

| Combined sense of hopelessness and helplessness, thoughts of disturbed family dynamics and financial instability along with feelings of loneliness, isolation and abandonment aggravates the sense of role dissatisfaction and conflicted feelings [Figure 1-2.2.a]. | …because it’s a question of survival.problems of finance, social, emotional…all the things are attached with it.and if you were the bread earner of the family…as I am in my case.you see that particular disease in everybody eyes in the family.every moment you meet your mother, your wife, your children.you can see cancer in their eyes (cried).it’s a living disease.it does not stick to my cheek or my mouth. I can feel it in my family. I can feel it in my friends. I can feel it in my circle.and then you become an object of…you know…where people say.alas, why you, you are such a good man…so where ever you go. you can feel the disease sitting there.it’s not limited to your body.you have to live with it…it becomes a living partner (cries).and I think at least for coming few years I will have to live with it (cries).although it would not be in my body…it would be with me…I’ll have to live with it (P-3) everyone is moving away.and getting distanced from me.because they know that I am not able to give them anything.(P-4) no one cares.if I die. people would come and cry.and then go back to work…(P-7) |

| Cancer to the bread earner plagues the thoughts with rehabilitation and survival issues. Academic and professional growth and career of children is hampered. Social stigma of disease and associated medical bankruptcy is a dual taboo [Figure 1-2.2.b]. |

kids…are school going.the school fee…other amenities for children…and that’s a major concern (P-2) Now, first of all the family has a mental (psychological) problem, because somebody in the family who is the bread earner…has disease…which is not.good. The survival.and getting him back in the same shape as he was. is a great concern for them.(P-3) …this disease is a taboo… people view this disease differently…moreover it impacts financial status so badly… you have to really think a lot about maintaining your societal status…(P-2) |

Rescue and relief factors (surviving the war)

Grown up, independent, earning children and other family members who are willing to help are huge pillars of support [Figure 1-3.1].

…children…are grown-ups.have their own jobs…there is no such burden.(P-1)

…family support is very important.this is a difficult time…their support matters…(P-1)

whole family is putting a joint effort in saving me.people have contributed money.(P-5)

Government panel beneficiaries need not pay from their pockets for a major part of treatment expenses (though not completely cashless for all) [Figure 1-3.2].

as far as treatment expenses are concerned, this hospital is listed in my official panel…otherwise the treatment is very costly…(P-2)

surely…helped a lot by the railways, otherwise I could not have got myself treated.(P-4)

.govt servant do get reimbursements for their treatment. But it is very difficult for self-employed people.(P-6)

Patients often wondered that had they not had insurance, they would have suffered financial agony and patient would have succumbed to disease [Figure 1-3.3].

but since I had already done…Medical Insurance… so we are relieved…else it would have been very difficult…very difficult…(P-1)

no I would not have been able to afford the treatment…I would have died.like many people do.die on the road.(P-4)

Learnings and innovations (lessons from the war; avoiding the next one)

Education and awareness are important especially for rural areas, where these could be done using government infrastructure and engagement with educated people as is done for election and voting purposes [Figure 1-4.1].

…nowadays children should also think similarly…people who are in private jobs…must first get their health insurances…(P-1)

we need to manage our assets…disease would not tell that its coming…it does not knock the door…(P-2)

healthcare is an industry…has a CSR (Corporate Social Responsibility), and that CSR is to educate the patients…(P-3)

govt school teachers, rural service officers and developmental officers…they should tell about insurances and govt schemes…other information related to banks, hospitals, policies…people really need it in the rural sector…(P-2)

Some patients came up with innovative ideas like loans on low-interest rates to cancer patients, staggered payments and crowd funding [Figure 1-4.2].

seeing the disease…interest rates should be lowered on loans…(P-2)

when you need to buy an electronic item… you could pay it in…instalments…but unfortunately, this kind of service or this kind of opportunity. is not available for such an important cause…(P-3)

start-ups and crowd funding are becoming a part of every industry. So, I think this medical industry should also go for certain type of crowd funding… wherein you get a certain amount from an existing patient, or a person who is not a patient…with a future commitment.(P-3)

I was reading of Narayan hrudyalaya, they tried to include the insurances thousand rupees a year…that could be another way of doing it…(P-3)

DISCUSSION

This qualitative study on adults in India with head and neck cancer clearly is first of its kind and clearly illustrates the multidimensional financial toxicity of cancer diagnosis and treatment, its short and long term repercussions, and various coping strategies used by the patients. Many of the findings are consistent with the limited studies in this area.[12212829]

Panic and preoccupation with working out the right diagnosis and line of treatment, finding out the appropriate place of treatment, and arranging finances for the same; takes the patient and their families through the cycle of multiple opinions, dilemma, finding resources; and finally landing up in an institution where the treatment starts.[23031] India has both government and privatized health-care sectors with >80% and 40% of outpatient and inpatient care respectively provided by the private sector hospitals.[4] Privatized health-care care costs are mostly paid either in cash, health insurances, or by panel reimbursements from the government departments. Patients reach a private set up either due to the fear of inadequacies in the government-funded hospitals or the thought that the facilities provided are better.[30]

Although high cost of cancer treatment is a well-known global phenomenon, an interesting finding in our study was the finding that initial diagnosis and treatment imposes an exponential cost in a short duration of time, which is particularly difficult to afford.[2930323334] It is compounded by inadequate reimbursements and healthcare insurances. Outpatient treatment and unsubsidized medicine costs are major contributors of the out of pocket cost burden, hence, the schemes which cover “only inpatient” hospital expenses are deficient in protecting against impoverishment.[3035] Awareness and education, lack of future visibility (and the idea of magnitude of financial burden which cancer could create) while planning health finances, poor social infrastructure, insufficient government policies and commercialization of health-care have increased the cost burden.[2830] Patients who travel long distances (or outstation) to reach the treatment facilities especially suffer more, both in terms of higher expenditures and advancement of the disease process. Various adjustments to mitigate the economic impact such as reducing expenses on children, travelling in overcrowded public transport (exposing themselves to infections) is like getting between a rock and a hard place.[3036]

Anxiety, financial insecurity, loss of morale, low self-esteem, threat to identity, and role dissatisfaction leaves the patient with mind-boggling survival issues and concerns about family economics after they die. Relationships see a lot of change from trivial difference of opinion/lack of support to cheating, fraud, abuse, and breakdown of the emotional bonds.[373839] All this, leads to a sense of loss of control, depression, stigma and existential distress.[740] Financial support from the family, employer reimbursements, and health insurances do offer some respite.[3041]

Though cancer is a health and financial catastrophe, it comes with its own set of learnings and opportunities to innovate; and propagate the change. It needs a right frame of mind and positivity of thoughts to learn from adversities and think out of box. The spectrum of this innovation spans right from advising newer ways of creating awareness, educating and preparing the society well in advance to deal with the financial catastrophe; to suggesting alternate methods of payment like EMIs; and to reduce the cost by crowd funding of latest equipment and machines. Identifying what “was” and “was not” in control and using that information to formulate financial coping strategies is a new facet, which we came across during this project.

CONCLUSION

This study is the first qualitative study from India focusing on financial toxicity from any kind of cancer. Besides the confusion and the loss of dreams associated with cancer, it puts a spot-light on the additional pain and suffering brought about by the financial stresses of trying to treat a disease which seems to drain the available family resources in its path. Clear information and early counseling of the families about costs, involving social support teams, and providing information on resources to help them cope would propagate good clinical practice. Innovative novel strategies need to be considered as the number of cancer patients and expenditure of modern treatment is only likely to grow further. Health insurance prioritization, early and goal based financial planning and adjustments for changing priorities at different points of time in life would come through public participation and efforts.

Like all other studies, we had our own share of limitations such as a small sample size, one urban private center which is not representative of all centers, not completely generalizable to other cancers as we have studied only head and neck cancers. A larger sample size and focus group interviews including immediate and wider family members, and social workers would contribute more to the understanding of this phenomenon. More investigation and research on this topic are needed.

Financial support and sponsorship

Nil.

Conflicts of interest

There are no conflicts of interest.

REFERENCES

- The growing burden of cancer in India: Epidemiology and social context. Lancet Oncol. 2014;15:e205-12.

- [Google Scholar]

- Series Cancer burden and health systems in India 3 Delivery of aff ordable and equitable cancer care in India Delivery of aff ordable cancer care in India: Global policy and national reality. Lancet Oncol. 2014;15:e223-33.

- [Google Scholar]

- Head and neck squamous cell carcinoma in young adults: A hospital-based study. Indian J Med Paediatr Oncol. 2019;40:18.

- [Google Scholar]

- Three Year Report of PBCR 2012-2014. Available from: http://www.ncdirindia.org/NCRP/ALL_NCRP_REPORTS/PBCR_REPORT_2012_2014/ALL_CONTENT/Printed_Versionhtm

- [Google Scholar]

- Economic burden of cancer in India: Evidence from cross-sectional nationally representative household survey, 2014. PLoS One. 2018;13:e0193320.

- [Google Scholar]

- Financial burden faced by families due to out-of-pocket expenses during the treatment of their cancer children: An Indian perspective. Indian J Med Paediatr Oncol. 2017;38:4-9.

- [Google Scholar]

- Financial burden of therapy in families with a child with acute lymphoblastic leukemia: Report from north India. Support Care Cancer. 2016;24:103-8.

- [Google Scholar]

- Cost of treatment for cancer: Experiences of patients in public hospitals in India. Asian Pac J Cancer Prev. 2013;14:5049-54.

- [Google Scholar]

- Cost analysis of in-patient cancer chemotherapy at a tertiary care hospital. J Cancer Res Ther. 2013;9:397-401.

- [Google Scholar]

- Understanding the full breadth of cancer-related patient costs in Ontario: A qualitative exploration. Support Care Cancer. 2016;24:4541-8.

- [Google Scholar]

- The financial impact of head and neck cancer caregiving: A qualitative study. Psychooncology. 2016;25:1441-7.

- [Google Scholar]

- Bridging the gap between financial distress and available resources for patients with cancer: A qualitative study. J Oncol Pract. 2014;10:e368-72.

- [Google Scholar]

- It's at a Time in Your Life When You Are Most Vulnerable: A Qualitative Exploration of the Financial Impact of a Cancer Diagnosis and Implications for Financial Protection in Health It's at a Time in Your Life When You Are Most Vulnerabl. Heal PLoS ONE. 2013;8:e77549.

- [Google Scholar]

- Addressing the financial consequences of cancer: Qualitative evaluation of a welfare rights advice service. PLoS One. 2012;7:e42979.

- [Google Scholar]

- Additional financial costs borne by cancer patients: A narrative review. Eur J Oncol Nurs. 2011;15:302-10.

- [Google Scholar]

- Identifying patients in financial need: Cancer care providers' perceptions of barriers. Clin J Oncol Nurs. 2009;13:501-5.

- [Google Scholar]

- Finding medical care for colorectal cancer symptoms: Experiences among those facing financial barriers. Health Educ Behav. 2015;42:46-54.

- [Google Scholar]

- The multidimensional nature of the financial and economic burden of a cancer diagnosis on patients and their families: Qualitative findings from a country with a mixed public-private healthcare system. Support Care Cancer. 2013;21:107-17.

- [Google Scholar]

- How illness affects family members: A qualitative interview survey. Patient. 2013;6:257-68.

- [Google Scholar]

- A critical appraisal of Kuppuswamy's socioeconomic status scale in the present scenario. J Fam Med Prim Care. 2014;3:3-4.

- [Google Scholar]

- Qualitative research: Standards, challenges, and guidelines. Lancet. 2001;358:483-8.

- [Google Scholar]

- Relationship vulnerabilities during breast cancer: Patient and partner perspectives. Psychooncology. 2009;18:1311-22.

- [Google Scholar]

- 'No matter what the cost': A qualitative study of the financial costs faced by family and whānau caregivers within a palliative care context. Palliat Med. 2015;29:518-28.

- [Google Scholar]

- Delivery of affordable and equitable cancer care in India. Lancet Oncol. 2014;15:e223-33. doi: 10.1016/S1470-2045(14)70117-2 Epub 2014 Apr 11. PMID: 24731888

- [Google Scholar]

- The socioeconomic and institutional determinants of participation in India's health insurance scheme for the poor. PLoS One. 2013;8:e66296.

- [Google Scholar]

- The financial burden and distress of patients with cancer: Understanding and stepping-up action on the financial toxicity of cancer treatment. CA Cancer J Clin. 2018;68:153-65.

- [Google Scholar]

- The high cost of cancer drugs and what we can do about it. Mayo Clin Proc. 2012;87:935-43.

- [Google Scholar]

- The high price of anticancer drugs: Origins, implications, barriers, solutions. Nat Rev Clin Oncol. 2017;14:381-90.

- [Google Scholar]

- Insured yet vulnerable: Out-of-pocket payments and India's poor KEY MESSAGES. Health Policy Plan. 2012;27:213-21.

- [Google Scholar]

- Financial toxicity, Part I: A new name for a growing problem. Oncology (Williston Park). 2015;27:80-149.

- [Google Scholar]

- The meaning of cancer: Implications for family finances and consequent impact on lifestyle, activities, roles and relationships. Psychooncology. 2012;21:1167-74.

- [Google Scholar]

- Clinical Social Work Journal the Hidden Cost of Cancer: Helping Clients Cope with Financial Toxicity.

- [Google Scholar]

- Physical, psychosocial, relationship, and economic burden of caring for people with cancer: A review. J Oncol Pract. 2013;9:197-202.

- [Google Scholar]

- Government Sponsored Health Insurance Schemes for Reimbursement of Cancer Treatment in India. Value Heal. 2016;19:A894.

- [Google Scholar]